For the first time in modern U.S. housing history, a 50-year mortgage is being seriously discussed on the national stage. With Donald Trump signaling support for ultra-long mortgage products during his previous policy proposals and campaign remarks, economists, investors, and everyday buyers are trying to understand one thing: How would a 50-year mortgage reshape the U.S. housing market?

The potential impacts of Trump’s 50-year mortgage on homebuyers stretch far beyond simply extending loan terms. This policy could influence affordability, market demand, long-term equity, interest-rate volatility, generational purchasing power, and even the structure of mortgage-backed securities.

In this in-depth guide, we break down how the policy may work, what it could mean for first-time buyers, where risks might emerge, and how tools like real estate analytics can help buyers make smarter decisions in a changing mortgage landscape.

What Is Trump’s 50-Year Mortgage Proposal?

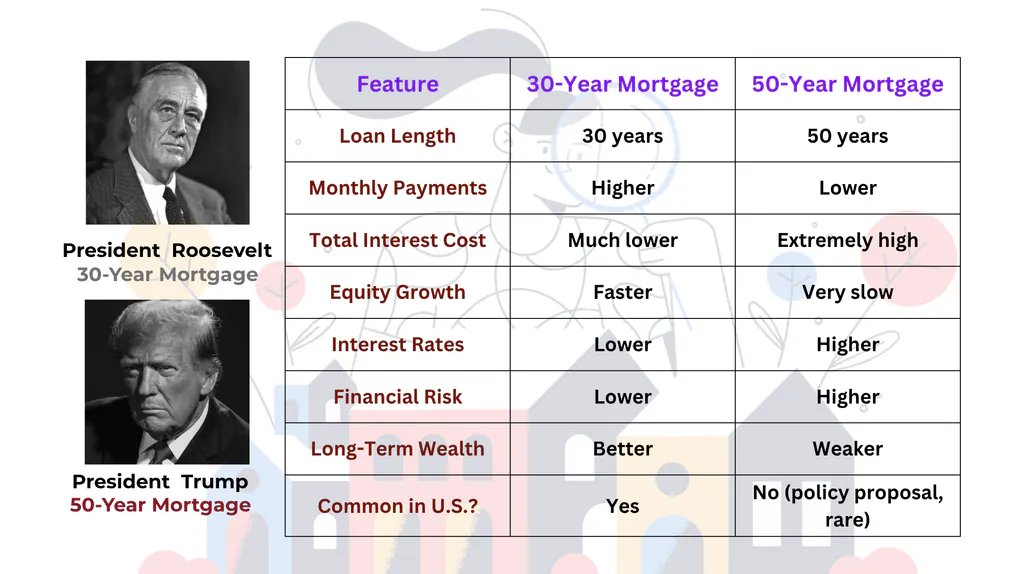

The idea of a 50-year home loan isn't real just yet, though talks about government backing for longer loans picked up speed between 2024 and 2025. Places such as Japan or the U.K. have been offering these kinds of deals for some time; meanwhile, limited tests happened in parts of America. Trump backing this idea lit a fire under folks wondering if homes can still be affordable. One upside? Payments each month drop big time with a 50-year loan. Yet, down the road, costs pile up - something anyone buying should get clear on. This is exactly why plenty of experts suggest checking property data tools before locking into a lengthy mortgage deal.

How a 50-Year Mortgage Would Change Affordability

One of the most immediate impacts of Trump’s 50-year mortgage on homebuyers would be a clear increase in monthly affordability. Stretching a loan from 30 years to 50 years could reduce payments by 20%–30% depending on the interest rate.

For example:

A $450,000 mortgage at 6.1% for 30 years results in a monthly payment near $2,720.

The same loan at 50 years could reduce the payment closer to $2,200.

This would open doors for:

First-time buyers priced out of the market

Younger households with limited income

Buyers in expensive markets like California, Washington, and New York

But lower monthly payments aren’t the full story. Extending a mortgage to 50 years means significantly more interest paid over time, and sometimes it can be hundreds of thousands more. Buyers need to use analytical software to model long-term outcomes before assuming a longer term is automatically better.

Slower Equity Growth

A big downside of a 50-year home loan? The main balance shrinks real slow. Actually, in the early decade or so, nearly all your payment covers interest instead. With a standard 30-year loan, the homeowner gains value much more slowly. That might affect:

Wealth-building potential

Risk exposure during market downturns

If house prices drop even 5–10% in a downturn, folks who’ve borrowed heavily with little down payment might end up owing more than their home’s worth. This is where high-quality analytical tools become essential. They help buyers forecast appreciation vs. amortization, so they understand whether they’re gaining value or just paying interest.

How It Could Affect Housing Demand

If Trump's 50-year mortgage spread across the country, home buying might spike - especially at first. Lower monthly costs could pull renters into owning houses instead.Still, higher demand might too:

Push house costs up even more

Heat up competition for homes in big cities

Reduce available inventory

Boost rivalry between buyers

We've noticed this trend earlier. Where cheaper loans came from tax breaks or short-term cuts, costs shot up fast 'cause everyone rushed to buy at once. So over time, homes could get less affordable if prices outpace paychecks.

Impacts on Real Estate Investors

Investors would be directly affected by a nationwide shift to 50-year mortgage options.

A few scenarios to consider:

More Competition for Entry-Level Homes

If buyers can qualify more easily, investors may have fewer distressed or undervalued homes to acquire.

Higher Rental Demand in High-Price Markets

In expensive cities, buyers may choose longer-term loans reluctantly, keeping rental demand stable.

Developers May Respond by Building More

Long-term mortgage accessibility could boost new construction, especially in the Sunbelt and Mountain West.

Using real estate analytics, investors can evaluate whether markets with extended mortgage terms are better suited for rentals or flips.

Will a 50-Year Mortgage Good for First-Time Buyers?

This is the biggest question of now days and the answer depends mostly on a buyer’s financial goals.

Potential Advantages

Opportunity to enter the market sooner

Flexibility for younger buyers with lower income

Potential Disadvantages

Higher total interest paid

Increased chance of negative equity

Longer timeline to pay off the home

First-time buyers must weigh short-term affordability against long-term financial stability. Using real estate analytics can help forecast future scenarios.

50-Year Mortgage Lead

Economists don’t agree. While some say looser mortgage rules push home prices up - much like in the 2000s bubble - others claim long-payment plans just adapt the economy to today's wages, aging populations, instead of outdated models. Still, rising property expenses play a big role either way. A recent study by the Urban Institute flagged risks tied to extended home loans - if handled poorly, they might lift costs quicker than paychecks grow, making housing tougher to afford.

This is why monitoring local conditions through real estate analytics is essential before assuming long-term loans are a perfect solution.

How Homebuyers Should Evaluate

With such a big decision, buyers need more than intuition, they need real and useful data.

Here’s how modern homebuyers can evaluate the impact:

Compare total lifetime interest costs using a mortgage amortization calculator.

Use analytical software to model appreciation rates.

Review neighborhood growth projections using real estate analytics.

Analyze whether refinancing later could offset long-term interest.

In markets where appreciation outpaces interest costs, a 50-year mortgage may be an acceptable tradeoff.

In markets with stagnant or declining values, it could be a costly mistake.

Conclusion

The possible effects of Trump’s 50-year mortgage on people buying homes might be huge - bringing fresh chances along with added dangers. For some, it could turn renters into owners, lower what they pay each month, or make pricey areas feel more reachable. On the flip side, building ownership stake might take longer, total interest over time could climb, maybe even spike up house costs across the board.

The main thing for any person buying a house is useful data and real Information. Looking at property data plus future trends helps you choose wisely - instead of going by feelings. Becoming a homeowner isn't only about paying each month; it's actually a long road to building value over many years.

FAQs:

1. Is a 50-year mortgage good for first-time buyers?

It can help reduce monthly payments, but buyers must consider slower equity growth and higher long-term interest.

2. Will Trump’s 50-year mortgage lower home prices?

Unlikely. Lower payments could increase demand and potentially drive prices up.

3. Can borrowers refinance a 50-year mortgage later?

Yes, refinancing to a shorter term is common when incomes rise or interest rates drop.

4. Are 50-year mortgages already available in the U.S.?

Only on a limited basis. Widespread adoption would require federal regulatory approval.

5. How can buyers evaluate the impact of a long-term loan?

Using real estate analytics and amortization models helps compare long-term costs and market conditions.