Key takeaways:

Plan your budget carefully around a single income by knowing what you can realistically afford, improving your credit score, and getting pre-approved early to avoid financial stress later.

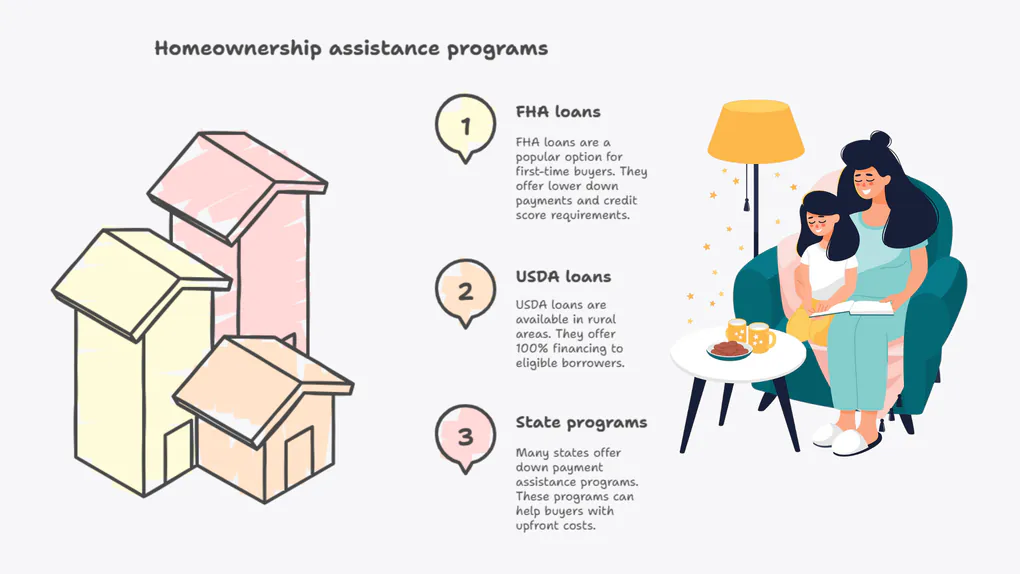

Use first-time buyer and assistance programs available in the USA such as FHA, USDA, and state-level down payment support to reduce upfront costs and make homeownership more achievable.

Prioritize long-term stability over short-term appeal by choosing safe neighborhoods, evaluating school districts, and factoring in maintenance and future expenses before buying.

Becoming a homeowner while raising kids alone in the U.S. might seem like too much. Juggling pay from one job, babysitting bills, time at work, and planning ahead - on top of tackling a major money move - can weigh heavy. Here’s the upside: plenty of moms doing it solo manage to close on houses yearly, so if you get ready well, this could be your path too.

Single women - like single mothers on their own - make up about 19% of home buyers in the U.S., beating out single guys, says the National Association of Realtors. The share keeps growing because loans are easier to get, help from the government is expanding, while lenders offer more adaptable deals. We’ll show you solid steps for single moms who want to buy a house here, using actual market facts, budget strategies, yet aiming for lasting security.

Know How Much House You Can Afford on a Single Income

A key tip for single mothers looking to buy a house in the U.S.? Figure out what you can afford - right from the start - so you don’t get hooked on dream homes that don’t fit your wallet. Since it’s just one paycheck, not two, your spending plan should play it safe, roll with changes, and hold up years down the line.

Lenders usually check your debt-to-income (DTI) number - this one shows how much you pay in debts each month compared to what you earn before taxes. While many standard lenders want that figure under 43%, some FHA loans might accept a bit more. Since home expenses keep going up, particularly in places such as California, New York, or Texas, keeping spending way beneath the top approved limit helps dodge money troubles.

A single mothers making $75K a year in Ohio might afford a house around $300K - yet going for one at $250K usually frees up cash for savings, kid care, or surprise expenses. Sticking to a tight budget boosts security down the road, particularly when times feel shaky economically, since homebuyers tend to hesitate while loan rates jump around.

You might get a clearer picture from this Pulse Real breakdown - shows how buyer trust stays shaky despite changes in U.S. home loan rates.

Save for a Down Payment and Use Single-Mother Assistance Programs

Saving up for a house might seem out of reach when you're living on one paycheck, yet many single mothers across America manage it by tapping into support options instead of relying only on what they’ve saved.

FHA loans need just 3.5% down, while USDA ones allow no money down if you're in eligible rural or suburban zones. Some state housing agencies give cash help made just for new buyers or solo mothers. In places such as Florida, Texas, or Illinois, these plans might hand out between $5K and $15K based on how much you earn and where you live.

Housing help from HUD’s main site shows current options per state - so many single mothers rely on this when thinking about buying a home. Instead of draining savings, many successful buyers keep a modest emergency fund intact and rely on assistance to bridge the upfront gap.

Improve Your Credit Score to Secure Better Loan Terms

Your credit score affects how much you pay each month, the interest rate, also your chances of getting approved. If you're a single mothers, fixing this could save you thousands over time.

Data from Experian suggests people who have credit scores higher than 740 usually get loan rates nearly 1% better compared to folks scoring around the middle 600s. On a three-decade home loan, this gap might add up to more than sixty grand in interest costs. Fixing your credit isn't about being flawless. Keep up with payments every month, bring card balances under thirty percent, or wait half a year without borrowing more before you apply - each step helps boost your number.

Get Pre-Approved for a Home Loan Early

Getting pre-approved isn't only about forms - it gives you sureness plus a clear picture. A key tip for single mothers looking to buy homes in the U.S.? Lock in approval before checking out houses.

Getting pre-approved shows how much a lender might give you after checking your pay, credit score, and savings. In busy areas such as Arizona or North Carolina, many home sellers toss out bids that don't come with this approval right away.

Some folks check out unusual payment plans when homes feel pricey - like stretching loans over more years. This report from Pulse Real dives into how these longer mortgages are shaping up lately.

Work With a Real Estate Agent Who Understands Family Needs

Some agents aren't the same - so if you're a single mothers, having someone who gets it really helps. Try finding one who's worked with new buyers before, knows about school districts, checks out neighborhood safety, or handles rules that apply nearby. A good buyer's rep isn't only about haggling cost - they pitch in by checking drive lengths, school options, plus how well the place might sell later. On top of that, they step in when talks get tense or inspectors show up, which keeps stress low through a tricky journey.

Research Safe Neighborhoods and School Districts Carefully

For single mothers, safety plus schooling usually aren't optional. Areas with less violence tend to hold property values better over time - FBI stats back that up. Checking out neighborhood crime patterns matters a lot before you decide. Pulse Real’s look at which states might see more crime by 2026 helps make sense of risks in different areas. Combining crime statistics with school district ratings often reveals neighborhoods that support both family well-being and property appreciation.

Define Must-Haves That Support Your Lifestyle

Space size isn't the main concern - what counts is how well it works. For many single moms, a smart setup beats fancy features; they go for good storage instead. Being close to schools or shops weighs more than extras like granite counters. Practicality wins every time.

A small bedroom close to schools or work could mean less stress over time compared to a bigger place that’s far away. Picking what matters first keeps spending under control while reducing rushed choices.

Tour Homes With Long-Term Affordability in Mind

Paint might look nice, yet real talk matters when single moms buy houses across America - think long-term upkeep. A roof that's seen better days, heating units stuck in the past, or walls that barely keep warmth could mean surprise bills piling up fast.

Some folks check if rent money can help cover expenses - especially with duplexes or backyard units. For smart tips on short-term rentals, hit up Pulse Real’s guide right here

Schedule a Home Inspection Without Exception

Missing an inspection could cost you big - especially if your budget runs on just one paycheck. The American Society of Home Inspectors says about 86% turn up something needing fixes. A check helps save money down the road - also gives you more power when bargaining.

Close With Confidence and Plan for Stability

Closing day isn't just forms - it's freedom, a fresh start. Go over your Closing Disclosure slow, check the bottom-line price, while making sure escrow amounts add up right.

Some single moms keep enough cash to cover bills for three or four months after closing - just in case, they go a bit under what’s fully approved.

Conclusion

The top house-hunting advice for single mothers across America? Get ready early, stay calm, take your time. Going at it solo isn’t going without help - because funding options, expert support, or smart research even things out.

Once you get your budget sorted, use available help programs, focus on safe areas, while planning ahead, buying a house turns doable instead of stressful. For moms raising kids alone, owning a place isn't only about money - it's about building security, strength, because it opens doors down the road.

FAQs:

1. Can single mothers buy a home with low income in the USA?

Yes. FHA, USDA, and state housing programs offer low or zero-down options combined with income-based assistance.

2. Are there mortgage programs specifically for single mothers?

While not labeled exclusively for single mothers, many first-time buyer programs effectively support them.

3. What credit score do I need to buy a house as a single mother?

FHA loans may allow scores as low as 580, while conventional loans typically prefer 620 or higher.

4. Is it better to buy or rent as a single mother?

Buying often makes sense if you plan to stay at least five years and monthly costs align with rent.

5. How much should I save for emergencies after buying a home?

Experts recommend three to six months of living expenses for stability.